Full Report

— — — — —

Summary

In summary, it appears to me that shares of Intrepid Potash are massively undervalued due to a disconnect in fundamentals. The issues driving that opportunity are complex, though; and have not yet been bridged by analysts and investors.

First there was the issue of distress—the Bet on Bob— which at this point is over. Finished. Complete. Dunzo! But for some reason, investors still don’t seem to fully believe it. The company’s core potash business is cash flow generative at current price levels and the balance sheet is nearly back to a net cash position. Intrepid is a company that will survive and compound capitallong into the future.

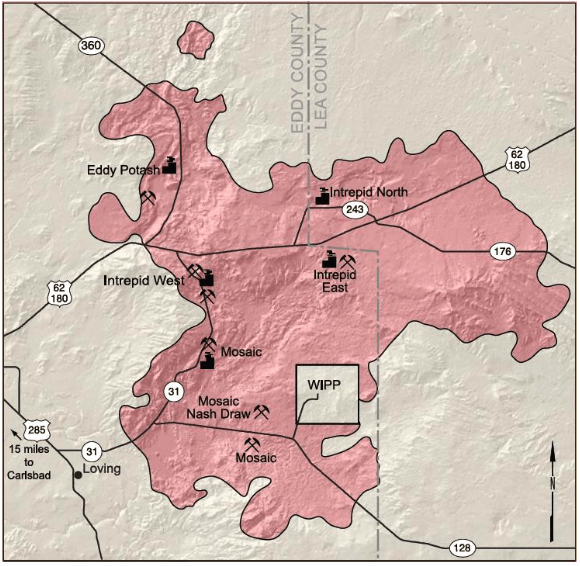

Next up was the issue of overcapacity—the Bet on Joc—which was depressing potash prices around the world. The sector pursued a price over volume strategy which has led to price stabilization and recovery. Agricultural commodity companies are trading near 52-week highs on expectations of continued momentum, yet Intrepid is not fully participating due to the drag from Trio and given misperception of its MOP production cash costs (GAAP vs. non-GAAP). While this makes sense, it has resulted in Intrepid trading at a significant discount to its fair value of $1b+, which I expect it to reach sooner rather than later.

And now there is the issue of water—the Bet on Blue—which has helped reignite excitement among investors, but has not yet fully materialized. Investors are going to be reading about the Permian basin for the next 50 years; and water may be the single, largest unresolved question among major producers in the region. There have been billions of dollars invested and billions more already allocated to ensure decades of production that may ultimately set the “marginal barrel” to control the entire industry. Demand for water could be staggering and Intrepid will be monetizing the value of water right assets for years to come. Whether this helps to “protect downside” or whether it provides a meaningful avenue for growth remains uncertain. But cash flow is real and on a discounted basis it is likely worth more than the entire current enterprise value of the company.

Something doesn’t add up, but it might just be that IPI is being priced far too low. This is the beauty of small-cap. Ephemeral moments of inefficiency that can lead to outsize returns. I expect 200-300%+ upside over the next few years, because by the time it becomes obvious it will be far too late.

That usually makes for a very good bet.